by Maireid Sullivan 2011, updated 2021

Work in progress

Note: Please refresh cache when revisiting these pages

Since WWII, US and UK Real Estate and Banking "Boom-Bust" cycles have peaked every 18 to 18.6 years: 1954, 1972, 1990, 2008 (& predicted for 2026/7), each with a mid-term recession. Australia varies a little.

Introduction

- Real Estate Speculation

-

Foreclosure Defined Part 1

-

Land Banking: This is how it works Part 2

- Learning from History: Kondratieff Wave explained Part 3

- Australia Part 4

- United States Part 5

- United Kingdom Part 6

- Ireland Part 7

- The Big Screen: chasing the money

Introduction

"If you don't tax that value that attaches to land, arising from the general wealth of the economy, the banks get it." – Michael Hudson, Professor of Economics at the University of Missouri–Kansas City and a researcher at the Levy Economics Institute at Bard College.

"What to do now? A strong dose of Georgist tax policy will revive the private sector of any city, and the surrounding rural areas too... [we need] a tax system that will compensate the losers from the gains of the winners." – Mason Gaffney (1923-2020), Professor of Economics, University of California, Riverside. (Obituary)

Real Estate Speculation - 2020/2040: STUDY PREDICTS MILLIONS OF UNSELLABLE HOMES COULD UPEND MARKET

Aug. 11, 2020, University of Arizona College of Architecture, Planning & Landscape Architecture (CAPLA) Professor Arthur C. Nelson's new research was cited in Consumer Affairs, Newswise, Phys.org and other outlets.

Excerpt: The prediction by CAPLA Professor Arthur C. Nelson undermines the classic "big promise" in homeownership: that a home, after it's paid off, can be sold for a retirement nest egg.

Millions of American homes could become unsellable -- or could be sold at significant losses to their senior-citizen owners -- between now and 2040, according to new research from the University of Arizona.

The study predicts that many baby boomers and members of Generation X will struggle to sell their homes as they become empty nesters and singles. The problem is that millions of millennials and members of Generation Z may not be able to afford those homes, or they may not want them, opting for smaller homes in walkable communities instead of distant suburbs. >>>more

Foreclosure Defined Source: Legal Dictionary . . . the system by which a party who has loaned money secured by a mortgage or deed of trust on real property (or has an unpaid judgment), requires sale of the real property to recover the money due, unpaid interest, plus the costs of foreclosure, when the debtor fails to make payment...

Australia

In Australia, if the mortgagor is unable to continue servicing the mortgage, a mortgagee’s auction is arranged, and the mortgagor is given notice to quit, while continuing to owe the bank the full amounts outstanding on loans.

There is a requirement that the bank should obtain the full market value of the property. If there’s more money raised at auction than satisfies the amount owed to the bank (including legal costs), the bank will deliver additional funds from the sale of the property to the mortgagor, or else the owner/mortgagor may be able to take legal action.

United States

Leading up to the 2008 "GFC"

American investment 'vulnerability' came to my attention at the peak of the "Celtic music wave" when, in response to the September 11, 2001 (9/11) catastrophe, banks introduced a short-term fixed interest strategy to encourage "Boomer" homeowners to re-enter the market, led by the ‘Bush-push': “Support the economy! Take a holiday! Build an extension! Buy a boat!”

Several personal friends, well-educated 'professionals’ took out a 2nd mortgage on their fully owned homes and had their mortgages ‘foreclosed’ when the 3-year fixed interest rates expired and variable rates were introduced: Their homes were taken from them, while first-time mortgage owners lost their home and their deposit, and they had to pay foreclosure legal costs.

“The greatest fine art of the future will be the making of a comfortable living from a small parcel of land.” - Abraham Lincoln

Land Banking: This is how it works Apartment developer billionaire Harry Triguboff, Australia's 2nd wealthiest man, as of 2011, was surprisingly candid at a lunch held by the American Chamber of Commerce in Oct 2011.

Triguboff told the audience he was able to pay “very little tax”...

“I keep a lot of my properties.

And if you keep them and there’s capital gain it’s beautiful,” he said. “You don’t pay tax. I don’t lease them so I don’t pay tax on the rent, but I get depreciation.” He paid tax on apartment sales but that’s where the land banking came in: “You have to buy lots of empty land,” he said. “You keep the land and it brings you no income, so you claim it against your tax.”

Source: Financial Review, 07 July, 2012.

(That article disappeared from the Financial Review as of mid-2016, but Leith van Onselen, at Macrobusiness, has shared a review here.)

Banks tranfer title deed:

Banks claim it isn’t their fault that they lost their 'business income' - their monthly mortgage payments - due to foreclosure. "They go through the legal process of getting the borrower off the title to the property and putting themselves on the title deed as the owner of the property" – Domnique Grubisa, Sept. 2020

In the lead-up to the 2007/8 GFC, in the US, Investment Bankers created a national crisis by gambling and loosing depositors savings due to the Stock Market Crash of August 2007. Consequently, US Treasury Secretary, 2006-2009, Henry "Hank" Paulson, (former Goldman Sachs CEO/Chairman), and Federal Reserve chairman Ben Bernake held secret meetings with Government regulators to negotiate federal intervention - to be “bailed out" by taxpayers.

Closing line from the 2015 movie, The Big Short,

referring to 2008/9 US government bank bailout:

"Paulson and Bernanke just left the Whitehouse.

There's going to be a bail-out. They knew.

They knew the taxpayers would bail them out.

They weren't being stupid. They just didn't care."

When it comes to 'following' Real Estate and Banking "Boom-Bust" Cycles, Australian economist Philip J. Anderson, author of the "The Secret Life of Real Estate and Banking" (2009), is a key expert on 'investment portfolios' and their history.

“Real estate is sold as a much safer investment than the constantly fluctuating stock market. Share price volatility is compared unfavourably with the steadier and impressive gains made from real estate which is, we are told, 'as safe as houses'. As millions of Americans – and countless others in the Western world - have recently found to their cost, house prices can also suddenly and dramatically drop. Yet no other text on real estate, either current or from the past, mentions this fact, reinforcing the perception that real estate is an almost risk-free investment.” – Phillip J. Anderson, (2009) "The Secret Life of Real Estate and Banking"

"Housing is a cost of living to wage earners. All outgoings associated with housing, including land taxes, are an attack on their cost of living." - Raymond Makewell, The Science of Economics, 2012 "...governments use the tax system to milk the poor. Why do they do it? To enrich people who own land." – Fred Harrison, Ricardo's Law, 2006

It would be easy to end 'investment' in real estate via taxation policy:

"Buying a house should be as easy as waking up in the morning and making a cup of tea." - John Tippett, A Philosophers Take on Economics, 2013

Investment strategist:

Preparing for The Next "Great Recession" - in Australia "Covid-19 will have an unpredicted impact!" On 18 March 2021, we heard from Roger Montgomery, Founder and Chief Investment Officer of Montgomery Investment Management, Australia: "Why I Think House Prices Will Keep Going UP"

This is what he said, in full-followed by selected readers comments:

“Australia is in the grip of its biggest property price boom in more than a decade. The boom is motivated in no small part by a fear of missing out. But there are also other important factors at play, leading me to believe that this trend could continue for some time.

Last year I outlined my bullish thesis for Australian property: cheap rates, a lack of stock and COVID losing its grip on the economy. But these all pale into insignificance compared to the impact of the easing of credit by banks if the government’s legislation relaxing responsible lending rules goes through.”

Three Comments on Roger Montgomery post:

1.

These trillions of fiscal dollars are quite different to the FED QE that only increased bank reserves. This is real money from nothing pumped into the community. The bond traders are onto it. I would not be so sanguine about interest rates.

2.

I think the last point on post covid migration will see this boom continue for many years to come…….50 year loans are just around the corner, that in my opinion, is one of the only ways (unfortunately) that our kids and grandkids will be able to afford to pay a mortgage into the future……

the bust, which will come eventually will be horrific!!!!

3.

A little off topic but recently my neighbours property sold by auction. As per normal operating procedure, the agent’s estimated guide wasn’t in the same solar system as the eventual sale price. Anyway, surely someone is working on disrupting this industry. How can they charge close to $70,000 to unlock a door 4 times? The wage increase of the beloved real estate agent must be 20% per year. I look forward to the day that the cost of selling a house isn’t so prohibitive.

To which, Roger Montgomery replied: "if the strong real estate prices persist there will be another agent ‘oversupply’ and most will be competing again for business."

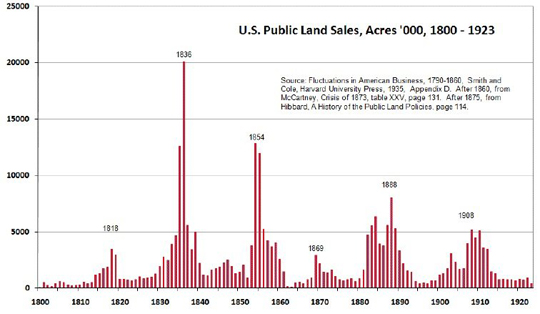

The 2007/8 Global Financial Crisis (GFC), stock market crash, should come as no surprise to history buffs. Philip J. Anderson shares an illuminating analysis of real estate bubbles through U.S. history.

The U.S. federal government began selling off land in the year 1800. "Since the 1800s, there have been peaks and valleys of land sales and speculation roughly every 18 years.

" - The Complete History Of US Real Estate Bubbles Since 1800. - Eric Goldschein, Buisness Insider, January 2012

“For the first 144 years of real estate enclosure in the U.S., land sales and/or real estate construction peaked almost consistently, every 18 years,” Anderson writes. “The world’s worst downturns are always preceded by land speculation (the chasing of the economic rent) fuelled by misguided credit creation courtesy of the banks.”

... "Rewind to the first major boom-and-bust, in 1837. The stock market peaked just prior to the bust, a trend we recognize in our own era. >>>more

Governments can align their policies with people's private goals

by abolishing anti-social taxes,

argues Bard University

Associate Professor of Economics Kris Feder.

Re-aligning behaviour to flow with the grain of both nature

and our human nature is achieved by removing the financial bias against those who work for their living.

"The financial sector has succeeded in depicting itself as part of the productive economy, yet for centuries banking was recognized as being parasitic. The essence of parasitism is not only to drain the host’s nourishment, but also to dull the host’s brain so that it does not recognize that the parasite is there. This is the illusion that much of Europe and the United States suffer under today. The aim of this book is to pierce this illusion and replace junk economics with economics based on reality. In Killing the Host, Michael Hudson argues that financial crises will continue unless we radically transform our economic and political structures, and reclaim the best ideas of classical economics."

KILLING THE HOST exposes how finance, insurance, and real estate (the FIRE sector) have gained control of the global economy at the expense of industrial capitalism and governments.

The FIRE sector is responsible for today’s economic polarization (the 1% vs. the 99%) via favored tax status that inflates real estate prices while deflating the “real” economy of labor and production.

The Great 2008 Bailout saved the banks but not the economy, and plunged the U.S., Irish, Latvian and Greek economies into debt deflation and austerity.

This book describes how the phenomenon of debt deflation imposes austerity on the U.S. and European economies, siphoning wealth and income upward to the financial sector while impoverishing the middle class.

Michael Hudson: Economists for the last 50 years have used the term “host economy” for a country that lets in foreign investment. This term appears in most mainstream textbooks. A host implies a parasite. The term parasitism has been applied to finance by Martin Luther and others, but usually in the sense that you just talked about: simply taking something from the host.

But that’s not how biological parasites work in nature. Biological parasitism is more complex, and precisely for that reason it’s a better and more sophisticated metaphor for economics. The key is how a parasite takes over a host. It has enzymes that numb the host’s nervous system and brain. So if it stings or gets its claws into it, there’s a soporific anesthetic to block the host from realizing that it’s being taken over. Then the parasite sends enzymes into the brain. A parasite cannot take anything from the host unless it takes over the brain.

The brain in modern economies is the government, the educational system, and the way that governments and societies make their economic policy models of how to behave. In nature, the parasite makes the host think that the free rider, the parasite, is its baby, part of its body, to convince the host actually to protect the parasite over itself.

That’s how the financial sector has taken over the economy. ...>>>more

20 Dec. 2020 The Law of Rent - Classical Political Economic solutions What is Rent Seeking? A Hard Look at Rent and Rent Seeking

with Professor Michael Hudson and International journalist Pepe Escobar

An interactive discussion on wealth inequality and the “Great Game” on the control of natural resources. In this webinar, Michael Hudson and Pepe Escobar unpack one of the most destructive features of our economic system and the many different ways it drives wealth inequality.

They also focus on China – US relations and their understanding of the “Great Game” regarding control of the world’s resources.

The Problem: How the Corrupt Purchase Luxury Real Estate in Key Markets Problem 1. Inadequate coverage of anti-money laundering provisions Problem 2. Identification of the beneficial owner of legal entities, trusts and

other legal arrangements is still not the norm Problem 3. Foreign companies have access to the real estate market

with few requirements or checks Problem 4. Over-reliance on due diligence checks by financial institutions

leads to cash transactions going unnoticed Problem 5. Insufficient rules on suspicious transaction reports and weak

implementation Problem 6. Weak or no checks on politically exposed persons and their associates Problem 7. Limited control over professionals who can engage in real

estate transactions: no “fit and proper” test Problem 8. Limited understanding of and action on money

laundering risks in the sector Problem 9. Inconsistent supervision Problem 10. Lack of sanctions

Executive Summary

The real estate market has long provided a way for individuals to secretly launder or invest stolen money and other illicitly gained funds. Not only do expensive apartments in New York, London or Paris raise the social status of their owners and enhance their luxurious lifestyles, but they are also an easy and convenient place to hide hundreds of millions of dollars from criminal investigators, tax authorities or others tracking criminal behaviour and the proceeds of crime. According to the Financial Action Task Force (FATF), real estate accounted for up to 30 per cent of criminal assets confiscated worldwide between 2011 a nd 2013.1

Several cases that have come to light in the past year, including the trial of Teodoro Obiang, son of the president of Equatorial Guinea;2 Malaysia’s 1MDB scandal;3 the Brazilian Car Wash Operation;4 and the Panama Papers’ revelations,5 offer examples of how high-end property in key markets may have been used to launder money. In many such cases, property is purchased through anonymous shell companies or trusts without undergoing proper due diligence by the professionals involved in the deal.

The ease with which such anonymous companies or trusts can acquire property and launder money is directly related to the insufficient rules and enforcement practices in attractive markets. The countries analysed in this study – Australia, Canada, the United Kingdom and the United States – have committed in different forums, such as through the FATF and the Group of 20 (G20), to do more to prevent and curb money laundering and terrorist-financing, including by regulating gatekeepers, such as real estate agents, lawyers and accountants, who may act as facilitators in transactions that can enable money laundering.

This report identifies the main problems related to real estate and money laundering in these four countries and finds that, despite international commitments, current rules and practices are inadequate to mitigate the risks and detect money laundering in the real estate sector. >>> more

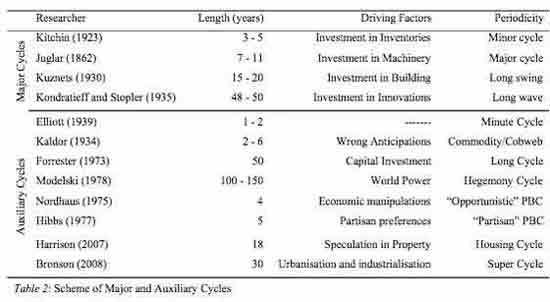

"Everything that happens once can never happen again. But everything that happens twice will surely happen a third time" - Coehlo (1999, p.164)

INTRODUCTION

The literature concerning business fluctuations reveals that there is a disagreement between classical and modern business cycle researchers on how regular business cycles are. According to Reiter and Woitek (1999), classical economists such as Moore (1914) and Kitchin (1923) saw business fluctuations as genuine cycles, i.e. recurrent phenomenon with typical characteristics. Conversely, modern macroeconomists including Zarnowitz (1992), Solomou (1998) and Dudukovic (2007) identify business cycles as a sequence of irregular fluctuations with no cyclical pattern. Dudukovic (2007) argues the term “cycle” is rather misleading, whereas business fluctuations do not tend to repeat at the regular time periods.As her evidences suggest, the length of business cycles, measured either from peak to peak, or trough to trough, vary substantially, implying that cycles are not mechanical in their regularity. Maddison (1991) and Solomou (1998) expressed similar views by stating that the average duration and other defining features of the business cycles have apparently changed over time. In the UK, these features changed notably after the 1970s, compared with the “golden age” between the 1950s and 1960s. Consequently, this variance of views and facts led macroeconomists, including Solomou (1998) and de Groot (2006), to hypothesise that over the years various types of cycles have been developed.The aim of this review is to explore the mechanics and rationale behind these cycles and thus argue the importance of the subject. The paper assesses what research methods, data and data analysis techniques were employed by researchers, and what were outcomes of these studies.

It is considered that a greater awareness of the various types of cycles discussed herein could be useful for both the private and public sector in assessing various economic issues. . . >>>more

Part 2

Learning from history: The Kondratieff Wave explained Back to top

Excerpt

“there is a category of scientists that leave after them a mystery that many others try to solve for many years, decades, or even centuries afterwards.

For two thousand years mathematicians tried to prove the Fifth Postulate of Euclid.

For three hundred years they were haunted by Fermat's Last Theorem. There are a number of such examples.

And the persistence demonstrated by scientists is not coincidental, for the discovery of the mysteries of harmony, be in nature or in the social life is the main goal of science.

The Russian economist Nikolay Dmitrievich Kondratieff left after him a mystery that has been haunting economists and social scientists for almost a hundred years. Joseph Schumpeter named this mystery ‘Kondratieff Cycles’. Why do we observe such regularity in long-term fluctuations of economic and non-economic indicators?”>>> more

In Kondratiev’s Paper on the Notion of Economic Statics, Dynamics and Fluctuations, published in 1924, Kondratiev’s conclusions were as follows.

1. Prosperity years were most common in the capitalist economies during upswing periods.

2. Agriculture suffered more and long depressions than did industry during price downswings

3. Major technological innovations were conceived in downswing periods but were developed in upswing periods

4. Gold supply increased, and new markets were opened at the beginning of an upswing

5. The most extensive and devastating wars occurred during periods of an upswing. –

3.

In 2001, Australian Taxation Office (ATO) Land Valuer Bryan Kavanagh made the case that short term interest rate cuts feed directly into higher and higher land prices and ever-escalating mortgages.

Follow his BLOG.

Excerpt:

NIKOLAI KONDRATIEFF (1892-1938?) was a senior economist in the Agricultural Academy and Business Research Institute under the regime of Joseph Stalin. His empirical analyses suggested that economic depressions occurred at relatively regular intervals. He considered 36 price, value and quantity series, including wholesale prices, interest rates, wages, foreign trade, industrial productivity and commodity prices since 1789 for the US, UK, France and Germany. Smoothing deviations from the trend in these data, he concluded thateconomies displayed long-wave cycles of between 54 and 60 years in duration.

Tragically, Kondratieff’s study apparently fell short of Stalin’s expectations. He was convicted of being a member of a secret peasants’ society and exiled in 1930 to imprisonment in Siberia, where he is said to have died.

Kondratieff did not attempt to give an explanation of the causality of the depressions determining the period of the longwave. He had shown only the approximate periodicity of the long-wave. Bryan Kavanagh argues that Henry George provided an explanation for economic depressions before Kondratieff demonstrated their approximate timing, and he explains why Australia, which is rich in the relevant real estate data, may be taken as a proxy for other industrialised nations when testing the current long-wave cycle. >>>more

Since 2016, Australian banks have been offering low-interest on 2 or 3-year fixed interest mortgages. As of 2021, banks are offering 1.75% on 3 year fixed rates.

EG, bank small print: After your Fixed Rate period ends, the applicable interest rate will be the variable Principal & Interest rate we offer on similar facilities at the time. Currently this is 2.34% p.a. for Owner Occupier loans and 2.74% p.a. for Investor loans. Rates, repayments and interest charges are indicative only and subject to change.

That's the big trap - proof that the NEXT "18.6-year Real Estate and Banking Boom-Bust Cycle" is still 'turning'. Historical formula suggests, with variations, an approximate "14 years to the top and 6 years to the crash" 14 years since 2007/8 = 2021/3 - the 'Turning'.

We're

on the way to the next crash, predicted for 2026/7.

There's uncertainty regarding the impacts of the Covid-19 'catastrophe'

- unlike the consequences of the 9/11 'catastrophe'.

The Global Financial Collapse (GFC) 2007-2008

January 2008: Australia's newly elected Labor Party Treasurer Wayne Swan revealed, on page 2 of his autobiography (2014), that US Treasurer Paulson telephoned him during the week he took office, in January 2008, to recommend he keep the real estate market 'UP'. Swan went on to launch the 'open door' policy for wealthy property investors; The Minerals Council of AU 'protected' the mining industry boom, while 'offshore' tax evasion continued.

Introduction

Has a generation been shut out of the Great Australian Dream?

It used to be that Australians would spend 3 or 4 times their annual income on a house. Now it's 10, 20, even 30 times, putting home ownership out of reach for many, and especially for young people. The tax breaks that have helped fuel the unprecedented housing boom will be a big issue in the coming election campaign. Taken together, Negative Gearing and Capital Gains tax breaks cost the public purse 11.7 Billion dollars each year. Labor has promised to wind-back the concessions. But despite criticism of Negative Gearing from some Liberal politicians, including former Treasurer Joe Hockey, PM Malcolm Turnbull has ruled out any changes to the system. In tonight's program, experts say that Australia's housing market is already cooling. Economists are divided over whether we're seeing the start of a soft-landing, a correction, or a crash. For many in the Millennial generation, a crash is what they're waiting and hoping for.

Excerpt: (38:00)

If the banks show the international investment community that they're lending to very, very credible borrowers -- credit-worthy borrowers -- then it's very, very easy for the banks to tap into very cheap debt and to be able to sell-off residential mortgage-backed securities with a triple-A rating. . . .

Housing is a cost of living for wage earners In a private email exchange, (quoted with permission),

Raymond Makewell, author of The Science of Economics (2013), stated: "Land only has a value (price) because the full economic rent is not being collected. The more economic rent (or land tax) that is collected the lower the price of the land. If the whole economic rent is collected the price of the land would be zero. The price (value) of improvements, though, could be negative. E.g. a site with a house on it that is approved for a block of flats: The existence of the house is a cost to any potential investor, not a benefit (i.e. the cost of removing the house). ...In a fully enclosed system, where wages are forced to the bottom, all taxation revenue comes from the economic rent. There is nowhere else for it to come from. If workers are taxed they demand higher wages or more government subsidies.

"Housing is a cost of living to wage earners. All outgoings associated with housing, including land taxes, are an attack on their cost of living. In the medium to long term collecting more economic rent on housing sites would reduce the price of land, but the immediate effect will be to increase wage demands, or government subsidies. The most effective action would be to concentrate on collecting taxation based on the economic rent from commercial sites, and reducing the overheads associated with employing people (income tax e.g.). The latter is intended to be provocative, but helpful."

Before the 2008 GFC, several warnings were issued by Australian Taxation Office (ATO) (Ret) Land Valuer and author Unlocking the Riches of Oz (2007), Bryan Kavanagh - is still 'following the cycles': Follow his BLOG.

"Although the facts are quite clear, economists sidestep this analysis, claiming that real estate bubbles are a factor of the under supply of land. Inadequate suitably zoned land explains these bubbles, they say, but they have no explanation for what caused land price bubbles before town planning and zoning came into existence, not all that long ago." - Bryan Kavanagh

YouTube:

(with Subtitles)

2005 Forecast of Global Financial Collapse

ATO Land Valuer Bryan Kavanagh, introduced by the Hon. Brian Howe AO, at Melbourne University, 2 August 2005, demonstrating why the world was about to experience financial collapse.

In May of 2007, Bryan Kavanagh published the results of his study on the long-term effects of property bubbles:

Synopsis:

This report collates Australia’s real estate sales since 1972 to create ‘The Barometer of the Economy’. As the barometer demonstrates a delayed inverse relationship between property bubbles and the economy, we investigate the extent of Australia’s publicly-generated natural resource rent in order to assess the scope for ‘Unlocking the Riches of Oz ’ currently suppressed by the deadweight costs of taxation. Re-calculating GDP on the assumption of the notional public capture of one half of Australia’s resource rent since 1972, we show the benefits that would flow to all Australians, the environment, housing affordability and industrial relations by reducing taxes in favour of greater reliance on resource rents to be substantial.

Mr Kavanagh's findings

According to Mr Kavanagh's study, collection of Resource Rent, aka Economic Rent, would allow Australia to remove all taxes on productivity, i.e. income, sales, pay roll tax – all business taxes.

Mr. Kavanagh's research revealed, in May 2007, that if the government collected half of Australia's 'Resource Rent' there would be,

1. Sufficient funding for all public services and public infrastructure, including free education and health care.

2. At 2007 value, an annual tax-free surplus-based 'Citizen Dividend' aka a 'Universal Basic Income' of between AUD$34,000. and AUD$49,000 would replace welfare, social security, and unemployment payments.

Commentaries by Bryan Kavanagh 1. Could it be that economists are ignorant of the Theory of Real Estate Valuation?

Bryan Kavanagh,

2012

i.e. that the phenomenon of land price is simply the capitalisation of its net annual rent? And, therefore, greater public capture of land rent via municipal rates and state land tax would keep the lid on recurrent land price bubbles? [...] The utter economic stupidity, hidden not only by neo-classical economists but also by the crass diversions in Australian political life, could of course be rectified by putting into place the recommendations of Ken Henry’s inquiry into the Australian tax system.

See full report, including illlustrative graphs HERE.

2. Property Bubble Leads to Crash Landing by Bryan Kavanagh

Featured in Business Age and The Sydney Morning Herald

Friday, March 28th, 2008

Excerpt:

Here is an unyielding truth. A country cannot go into recession unless there has been a real estate bubble.

US land economist Homer Hoyt documented the fact back at the beginning of the 19th century.The Land Values Research Group recently defined and studied the effects of property bubbles inUnlocking the Riches of Oz: A Case Study of the Social and Economic Costs of Real Estate Bubbles, 1972 to 2006, which is freely available at www.lvrg.org.au. It concludes that the current residential bubble has hyper-inflated since 1999 and is about to burst, despite sophisticated financial derivatives, hedge funds, collateralised debt obligations, credit default swaps, all brought into existence to “insure” that it not burst. The failure of derivatives will compound the upcoming financial threat.>>>more

Bryan Kavanagh contributed key research

under the auspice of the Land Value Research Group Founded in 1943, the LVRG published world-leading empirical studies demonstrating that site-value rating —that is, the imposition of municipal Rates on land values alone, exempting the values of buildings —is more conducive to economic growth than alternative systems that include buildings in the tax base. Expressed in qualitative terms, that conclusion should be obvious: taxing buildings deters construction and consequently impedes the industries that lie upstream or downstream of construction or require accommodation for workplaces and workers —in other words, it impedes the whole local economy —whereas taxing the value of land cannot reduce the supply of land, because neither the land nor its value is produced by the owner. Excerpt:

In 1943 the Canadian land economist H. Bronson Cowan, director of the International Research Institute on Real Estate Taxation, visited Melbourne to conduct research in the municipalities of Brunswick and Camberwell. His techniques inspired a number of local professionals to form the Land Values Research Group (LVRG). Under its founding director, Allan R. Hutchinson BSc MIEAust (1907–1988), the LVRG published 37 major documents.>>> more

Stupid Property Owners By Dr. Gavin Putland,

Director, Land Value Research Group January 2009 "The 'taxes' that property owners hate most are the ones that hurt them least and are most likely to be spent for their benefit." - Dr Gavin Putland

Excerpt:

Land and taxes In any tax jurisdiction, the supply of land is fixed. From the viewpoint of the taxpayer, the supply of land zoned for any particular purpose is also fixed, as is the supply of land within acceptable distance of any particular services, infrastructure, or markets. Yet access to suitably located land is essential to economic participation. Therefore land values, expressed as rent or as interest on purchase prices, are competed upward until they absorb the economy's capacity to pay. As that capacity increases — as it usually does — so do land values [1]. That's why economic growth doesn't make housing more affordable. That's why we load ourselves with debt in order to “own” our homes as soon as possible. This much is obvious even to the unschooled; they may not know anything about economics, but they know where their money goes.

Most taxes target transactions (or the results thereof), causing otherwise viable transactions, hence otherwise viable enterprises and industries, to become unviable. In this way, most taxes take far more money out of the private sector than they deliver to the Treasury (and thence back to the private sector through public spending). The margin by which the cost to the private sector exceeds the benefit to the Treasury is what economists call the excess burden or deadweight cost of taxation. In simple terms, most taxes take more than they give.

>>> more

Following the September 11, 2001 (9/11) catastrophe -

Banks introduced a short-term fixed interest strategy to encourage "Boomer" homeowners to re-enter the market, led by the ‘Bush-push': “Support the economy! Take a holiday! Build an extension! Buy a boat!”

Several personal friends, well-educated 'professionals’ took out a 2nd mortgage on their fully owned homes and had their mortgages ‘foreclosed’ when the

3-year fixed interest rates expired and variable rates were introduced: Their homes were taken from them, while first-time mortgage owners lost their home and their deposit, and they had to pay foreclosure legal costs.

Looking back, from Noam Chomsky's perspective:

“Manufacturing Consent: Noam Chomsky and the media” (1992)

Following the 1987 Stock Market crash, Chomsky's film credits celebrated the accumulating effects of community-based initiatives - local newsletters/papers, community radio and tv stations supporting an international popular outpouring of collaborative 'community activism'.

Withdrawal as a survival strategy

Palliatives for cultural withdrawal

Addiction and consumerism

Alienation and division

Interpretation and perception is everything.

Concepts such as Post Modernism, Consumerism, and Globalization defined cultural meanings as numerous and fragmented, rather than an homogenous construct (e.g. the American culture or the European culture). Consumer culture was viewed as a social arrangement in which the relations between lived culture and social resources, between meaningful ways of life and the symbolic and material resources on which they depend, are mediated through market.

– Arnould, E. J. (2005). Consumer culture theory (CCT): Twenty Years of Research, Journal of Consumer Research

"The cost to construct a given house is roughly the same in any region or metropolitan area of the United States. Yet, in the places were economic activity is robust and population dense, the land component of a residential property can equal 50 percent or more of the purchase price of a property. This occurs because the rent of land is lightly taxed and is therefore capitalized by market forces into a selling price, a selling price driven upward by speculation, hoarding and liberal access to credit. Henry George rightly observed that the rent of land should be fully collected by society to pay for public goods and services, leaving capital goods (e.g., buildings, homes, machinery) unburdened by taxation. If this was done, he felt confident there would be no need to tax income or commerce."

– Edward Dodson, economist and political scientist, and curator at

The School of Cooperative Individualism.

Corruption of Economics

Professor of Economics at University of California, Riverside since 1976,

Mason Gaffney (1923-2020), co-authored (with Fred Harrison and Kris Feder) the authoritative documentation of The Corruption of Economics (1994) – a detailed history of the suppression of Classical Political Economic theorem in favour of the current neo-classical speculative system, to reveal the precise manner in which Classical Political Economic theorem was 'neutralized':

In short,

(i) economic modelling became fundamentally corrupted via blurring of the traditional distinction between capital and land and hence between earned and unearned income,

(ii) by glossing this blurred distinction with jargon and abstract models, and

(iii) by recasting economics generally to make free-riding by landowners seem just and moral. See excerpt here.

Before the 2008 GFC

Not much fizz left in the global economy

by Stephen Roach, Chief Economist of US investment bank Morgan Stanley

Financial Times, August 14, 2006

Excerpt:

There is nothing like the seduction of a boom. The recent vigour of global economic growth is a siren song. By International Monetary Fund metrics, world gross domestic product growth probably averaged 4.8 per cent over 2003-06, the strongest four years since the early 1970s. As tempting as it is to extrapolate this into the future, that may be a serious mistake. There is a much better chance that global growth has peaked and the boom is about to fizzle.

The world’s main growth engine, the US, is slowing. That is the verdict from the labour market, with job growth in the past four months running 35 per cent below average since early 2004. It is the verdict from the housing market, where an emerging downturn in residential construction activity is knocking at least 1 percentage point off the GDP growth trend of the past three years. And, notwithstanding July’s temporary bounce-back in retail sales, it is a message from the consumer, whose inflation-adjusted spending growth fell to 2.5 per cent in the spring period – one percentage point below the heady trend of the past decade.

The US Federal Reserve is under fire - again. CNBC Business News' Rising Risks reporter Diana Olick shares her comprehensively informative overview.

KEY POINTS

• Home prices nationally in January were up 11.2% year over year, according to the latest S&P CoreLogic Case-Shiller Index. That is the largest annual gain in nearly 15 years.

• As of last week the Federal Reserve held $2.2 trillion of agency mortgage-backed securities.

• "They've continued on autopilot. I don't think there's been any discussion within the Fed," said Peter Boockvar, chief investment officer at Bleakley Advisory Group.

Home price gains are accelerating at an alarming pace, fueled by Covid pandemic-related inflation, which some claim is not getting enough attention from the Federal Reserve.

Home prices nationally in January rose 11.2% year over year, according to the latest S&P CoreLogic Case-Shiller Index. That is the largest annual gain in nearly 15 years.>>>more

Excerpt:

Our latest Nobelist in economics, Thomas Schelling, offered the following advice in the wake of Hurricane Katrina: “There is no market solution to New Orleans. It is essentially a problem of coordinating expectations. . .” By that he meant simply that each person’s incentive to move home and rebuild depends on his or her confidence that others will do likewise. “But achieving this coordination in the circumstances of New Orleans seems impossible.”

. . .

Historians have obsessed over the quake and fire but blanked out the recovery. We do know, though, that in 1907 San Francisco elected a reform mayor, Edward Robeson Taylor, with a uniquely relevant background: he had helped Henry George, more than anyone else, write Progress and Poverty in 1879. George, of course, is the one who wrote and campaigned for the cause of raising most revenues from a tax on the value of land, exempting labor and sales and buildings. (See "A Primer on Henry George's Single Tax.")

In 1907, single-tax was in the air, and it was natural to go along with Cleveland (Mayors Tom Johnson and Newton Baker), Detroit (Mayor and later Governor Hazen Pingree), Toledo (Mayors Samuel "Golden Rule" Jones and Brand Whitlock), Milwaukee (the "sewer socialists" and Mayor Dan Hoan), Chicago (Mayor Edward F. Dunne, ex-Governor J.P. Altgeld, muckrakers Ida Tarbell and Henry D. Lloyd, editor Louis F. Post, Nobelist-to-be Jane Addams, Councilman Clarence Darrow, et al.), Vancouver (six-time Mayor Louis Denison "Single-tax" Taylor), Houston (Assessor J.J. Pastoriza), many smaller cities, and doubtless other big cities yet to be researched, that chose to tax buildings less and land more. It was the golden age of American cities when they grew like fury, and also with the grace of the popular "City Beautiful" motif.

San Francisco bounced back so fast its population grew by 22% from 1900 to 1910, in the very wake of its destruction; it grew another 22% from 1910 to 1920 and another 25% from 1920 to 1930, becoming the tenth largest American city. It did this without expanding its land base, as rival Los Angeles did, and without stinting its parks. On its steep gradients it housed, and linked with publicly-owned mass transit, a denser population than any city except the Manhattan borough of New York. It is these people and their good works that made San Francisco so famously livable, the cynosure of so many eyes, and gave it the massed economic power later to bridge the Bay and the Golden Gate, grab water from the High Sierra, finance the fabulous growth of intensive irrigated farming in the Central Valley, and become the financial, cultural, and tourism center of the Pacific coast.

Mayor Nagin of New Orleans tells the world that Katrina wiped out most of his tax base, so he is impotent. By contrast, in 1907 Mayor Taylor's Committee on Assessment, Revenue, and Taxation reported sanguinely that revenues were still adequate. How could that be? Because before the quake and fire razed the city, land value already comprised 75% of its real estate tax base. San Francisco also taxed "personal" (movable) property, but it was much less than real estate, and secured by a lien on land. The coterminous county and school district used the same tax base. They also made extensive use of special assessments on lands benefited by specific public works. In other words, San Francisco had adopted most of Henry George's single tax program de facto, whether or not they said so publicly.

It was a jolt to replace the lost part of the tax base by taxing land value more, but small enough to be doable. This firm tax base also sustained the city's credit, allowing it to finance the great burst of civic works that was to follow. Taylor supported the next mayor but one, James Rolph (1911-1930), who oversaw a long period of civic unity and public works. "Sunny Jim" Rolph expanded city enterprise into water supply, planning, municipally owned mass transit, the Panama-Pacific International Exposition, and the matchless Civic Center. Good fiscal policy did not turn all the knaves into saints: Rolph eventually fell into bad company with venal bankers and imperialist engineers. But San Francisco rose and thrived. ...

At the turn of the last century, Henry George and the "Single Tax" movement he inspired were household names. George's 1879 book Progress and Poverty captured the imagination of millions in the United States and elsewhere, who found in his ideas a blueprint for an economic system that would retain capitalism's productive dynamism and distribute its fruits more fairly.

To summarize George's political-economy: George began from the premise that the land, along with all other natural resources, is the common inheritance of all. No persons or firms should own land; they should only be able to rent it. Furthermore, that rent should be paid to the public, as the rightful collective owner of all land.

Individuals and firms should own entirely whatever results from their efforts to make the land productive, however, whether by farming it or building a factory on it. They should also own entirely whatever profit they can create through the investment of accumulated capital. (In other words, George was not a socialist.)

The single-tax program was George's plan for implementing this view. The "single tax" was to be a property tax, on land but not on improvements, at a rate high enough to provide adequate revenue to the government. These tax payments would represent the "rent" those who use the land owe to the public. At the same time, taxes on labor income and on capital earnings would be eliminated.

George argued that the single-tax program would boost the economy. A sound economic system encourages both work and capital investment, so governments should avoid taxing labor income or returns on capital. At the same time, a productive system discourages rentier behavior?holding onto resources like land, living off of rents or waiting for speculation to raise land prices. With a high property tax, he believed, land will tend to end up in the hands of those who can make it most productive.

Echoes of George's ideas can be found in many strains of progressive economic thought today. For example, activists have proposed creating a so-called Sky Trust that would collect fees from firms that emit carbon dioxide. These firms are using up our common inheritance of a low-CO2 atmosphere, Sky Trust proponents argue, so they owe the public a "rent" that would serve as both an incentive to clean up their emissions and a source of funds for environmental protection efforts or "dividend" payments to the public.

Scottish economist and philosopher Adam Smith (1723-1790), the reputed founder of Classical Political Economics, visited the Physiocrats in France while touring across Europe (1764-1766) as tutor to a young Scottish nobleman, Henry Scott, 3rd Duke of Buccleuch. Smith was influenced by the Physiocrats' economic theorem:the wealth of nations was derived solely from the value of land agriculture or land development.

Ten years later, Classical Political Economics theorem was formally launched with Adam Smith's publication of "An Enquiry into the Nature and Causes of the Wealth of Nations" (1776), aka The Wealth of Nations.

"The rent of land, therefore, considered as the price paid for the use of the land, is naturally a monopoly price. It is not at all proportioned to what the landlord may have laid out upon the improvement of the land, or to what he can afford to take; but to what the [tenant] can afford to give." – Adam Smith, William Playfair, Dugald Stewart, An Enquiry into the Nature and the Causes of the Wealth of Nations, 1818 Ed, Vol. 1, CH XI, p. 104 (Google Book scan)

Ricardo's Law British Political Economist David Ricardo, (1772-1823), who defined the income derived from the ownership of land and other free gifts of nature as "The Law of Rent" (aka Economic Rent, Ricardo's Law, Resource Rent), with collection methods referred to as Single Tax | Resource Rent | Land Value Tax | Site Value Tax, and more: A philosophy and economic theory that follows from the belief that although everyone owns what they create, land, and everything else supplied by nature, belongs equally to all humanity.

“… without a knowledge of [the law of rent], it is impossible to understand the effect of the progress of wealth on profits and wages, or to trace satisfactorily the influence of taxation on different classes of the community” – David Ricardo

Summary excerpt:

This book offers the first comprehensive assessment of Tony Blair’s premiership and his Third Way project. It reveals the hidden flaw in the market economy which explains why politicians, of all parties, cannot keep their grand promises.

Blair promised to reform the Welfare State – the pact between people and their governments to abolish the evils of poverty and ignorance. In fact, however, despite a record three election victories in a row, the gap between rich and poor widened. The reason, the author argues, is the method government relies on to raise taxes. Contrary to intention, the tax burden on low-income earners increased, while property owners have enjoyed record capital gains. The outcome is over £1trillion indebtedness which renders tens of thousands of families vulnerable to bankruptcy and the loss of their homes in the next recession.

Fred Harrison reveals how taxpayers’ money is channelled behind the scenes, through ‘the invisible hand’, from poor to rich people and from poor to rich parts of the country.

Public spending, for example on roads, railways, schools and hospitals, makes a major contribution to rising land values. These benefit house and other property owners, rich ones more than poor ones, desirable locations and asset-rich parts of the country more than poor ones, but those who rent their properties do not share in the windfall gains. In fact, they have to pay rising rents.

Taking Britain as a case study, Harrison escorts the reader along an old Roman road from south to north to pin-point how poverty is institutionalised in the growing divide between rich and poor. Along the way he illuminates the inner workings of tax policies and property rights that similarly afflict all market economies. >>>more

UK House of Commons seminar on land value April 2009: Organised by The Coalition for Economic Justice

The seminar was aimed at parliamentarians and policymakers and examined the advantages of land value taxation, how it might be introduced and how transitional problems could be dealt with.

Hosted by Vince Cable MP

Panel of Speakers:

Prof Iain McLean, Professor of Politics, Oxford University

Ashley Seager, The Guardian

Molly Scott Cato, Green Party Economics speaker

David Triggs, Henry George Foundation

Sir Sam Brittan, Financial Times

Fred Harrison, Land Research Trust

Read the full report here

Excerpts:

As Sir Sam Brittan saw it, the case for LVT was clear and simple. But perversely, people find this difficult to grasp; they expect complexity in taxes. Being a tax on unearned value increment, LVT was no disincentive to Labour or Capital. As a temporary expedient, pending the full introduction of LVT, he advocated the auctioning of planning permissions.

Ashley Seager of The Guardian cited instances where public expenditure had led to massive increases in property (i.e., land) prices. In one case, the building of a school had led to such a big increase in local property prices that teachers in the school could not afford to live in the area. As the land of this country is provided free of charge by nature, “rising property prices do not raise national wealth one single penny”. They serve no useful economic purpose and are an obvious target for taxation.

Professor Iain McLean explained how, as a member of the independent expert group set up by the Calman Commission, he was looking at LVT as a way of financing public services in Scotland and Wales. LVT would replace council tax, business rates and stamp duty.

From a Green perspective (Molly Scott Cato), land is a trust for the people, its life-giving properties to be preserved from one generation to the next. LVT, which aims to curb private profiteering from the nation’s patrimony, was seen as a valuable tool in this connection.

The groundwork for the panel discussions was set out by David Triggs in his opening address. “The challenge that confronts those interested in establishing a just and equitable division of the fruits of production lies essentially in recognising that land values impound that part of the value created which is attributable to factors external to the individual, e.g., the country’s infrastructure, the system of governance, law and order and the density of population. It is manifestly unfair to tax the individual on what he produces while those community-created values are provided tax-free to the benefit of the landowner. These land values, arising essentially from location, should be the primary source of taxation.”

Fred Harrison reinforced this message. He showed how failure to collect location value led to diminished opportunity and life expectancy at the marginal location.

James Black (a sixth-former) said LVT made common sense to the young and the opportunity should not be missed. >>> more

2.

In June 2005, Bryan Kavanagh, Land Valuer, Australian Taxation Office, wrote a letter to The Age, Melbourne, which was published on June 15, 2005:

Resource rents hold the property key Analysts and policymakers may learn a valuable lesson from the history of Ireland" by Bryan Kavanagh Land Valuer, Australian Taxation Office

June 15, 2005 The Age Newspaper

Excerpt:

. . . Both Cromwell and Petty saw the need to know the annual value of Ireland's natural resources, but the modern neo-classical economist is all but clueless on the quantum of resource rent within the economy, or for that matter to where it disappears. . . .

The Russian economist Nikolai Kondratieff did not have an explanation for the cause of the 50 to 60-year-long wave cycles he discovered in his studies of 140 years of the economies of the US, Britain, France and Germany. However, cycles of boom and bust seem to be inextricably linked to the failure of economies to capture the national rent for their coffers, and to the consequent escalation in land prices and taxes levied on productive work. Where most modern economic analysts don't like to acknowledge the existence of the Kondratieff wave because it is suggestive of their impotence during its deflationary decline, it is possible to clearly show the inflationary, then deflationary, courses of the fourth Kondratieff wave within the economies of Australia, the US and Britain. The end of each of the three preceding long waves was defined by economic depression. ... Whereas it was accepted in Petty's day that the annual rent of land was a surplus that came about by the mere existence of community, and its collection and use was the cheapest and most equitable source of revenue, we are now educated to forget that. As the annual value of our natural resources is privately expropriated, it has become necessary to levy myriad taxes on all sorts of productive activities. – Bryan Kavanagh, Land Valuer (Ret.), Australian Tax Office

Mr Kavanagh's complete 2005 letter is shared HERE.

Index

Introduction

Open Letter from nine Irish academics

- Overview

- A big constitutional mistake

– Part 1

European Community

- Irish Foreign Policy

- Irish Military Neutrality

– Part 2

Cultural Tourism

– Rise of the Celtic Tiger

- Hindsight on Cultural Tourism policies

– Part 3 Consumers: Not Citizens

- Written into the constitution of the Euro-zone

- Lisbon Treaty 'Guarantees'

– Part 4 How the Banks captured Ireland too

- Stephen Donnelly, TD, Four conversations ...

- German perspectives

- Brexit

– Part 5 Caught in the middle - Collapse of the Celtic Tiger

- Killing the Celtic Tiger

- Land Value Taxation in Ireland

- The Fair Tax: Supported by History,

Agreed by Economists, Feared by the 1%

– Part 6 Why would Ireland give away its natural resources?

- Three urgent issues

Inside "Predatory Capitalism"

- where anyone can 'make it big'!

'Must see' films:

Glengarry Glen Ross (1992), inside the Real Estate business:

"The drive for capital gain has dehumanized us." Starring Al Pacino, Jack Lemmon, Alec Baldwin, Alan Arkin, Ed Harris, Kevin Spacey, Jonathan Pryce. An examination of the machinations behind the scenes at a real estate office: The desperation to make money, preying not only on customers, but on each other.

Wall Street (1987),

leading to Wall Street: Money Never Sleeps, (2010).

Both films were directed by Oliver Stone and co-written by Oliver Stone and Stanley Weiser, who claim that the lead character, Gordon Gekko (played by Michael Doublas), is based on a composite of real-life financiers - corporate raider Carl Icahn, disgraced stock trader Ivan Boesky, and investor Michael Ovitz.

“Money never sleeps, pal” ... "greed, for lack of a better word, is good. Greed is right, greed works. Greed clarifies, cuts through, and captures the essence of the evolutionary spirit. Greed, in all of its forms; greed for life, for money, for love, knowledge has marked the upward surge of mankind."

- Gordon Gekko, played by Michael Douglas (More quotes here)

'insider' banking short list:

Wall Street (1887), followed by Wall Street: Money Never Sleeps (2010); Inside Job (2010); Too Big to Fail (2011); Margin Call (2011);

The Wolf of Wall Street (2013); 99 Homes (2014); The Big Short (2015); Miss Sloane (2016); Vice (2018);

Too Big to Fail (2011) is an adaptation of the 2009 book by New York Times journalist Andrew Ross Sorkin, "Too Big to Fail: The Inside Story of How Wall Street and Washington Fought to Save the Financial System --and Themselves".

Based on the 2010 book by Michael Lewis “I would read an 800-page history of the stapler if he wrote it.”

— John Williams, New York Times Book Review)

Lead character, Mark Baum, played by Steve Carell portraying famed investor Steve Eisman, who profited on the 2008 housing crisis by shorting subprime mortgage loans, and now sees opportunity in large US banks. >>>more

The global financial crisis of 2008, which economists estimate could result in several trillion dollars of losses and which has already cost American taxpayers billions of dollars in government bailouts, was triggered not by war or recession but by a crazy, man-made money machine, built on flawed mathematical models that most financial executives did not really understand themselves. Greedy and heedless, Wall Street firms had been turning subprime mortgages loans made to people with low credit worthiness or little documentation into exotic, toxic financial products that they made a fortune laundering and reselling, and they were enabled in doing so by the very ratings agencies that were supposed to police risk. >>> more

IMDB: Storyline: Three separate but parallel stories of the U.S mortgage housing crisis of 2005 are told:

-

Michael Burry, an eccentric ex-physician ... believes that the US housing market is built on a bubble that will burst within the next few years.…

"Four denizens of the world of high-finance predict the credit and housing bubble collapse of the mid-2000s, and decide to take on the big banks for their greed and lack of foresight."

Summary: The Big Short (2015)

The GFC was announced on September 8, 2008 with news that Bear Stearns and Lehman Bros had collapsed due tomarket volatility in world economy.

In the USA, 5 Trillion dollars in pension money, real estate value – GONE –

401K, savings and bonds had disappeared.

8 million people lost their jobs.

6 million lost their homes.

Michael Burry, MD, the medical doctor who was the first to 'see' "the hedge fund opportunity" has since been audited 4 times and questioned by the FBI. He now invests in WATER!

Banking on spin: In 2015, several banks started selling billions in "bespoke tranche opportunities" aka CDO (Bloomsberg News)

Selected excerpts:

"It's possible that we're in a completely fraudulent system."

– Mark Baum, (aka Steve Eisman) played by Steve Carell

Mark Baum's conference lecture, presented at the moment the collapse, was beginning to unfold: "We live in an era of fraud in America -- not just in banking, but in government, education, religion, food - even baseball. What bothers me isn't that fraud is not nice or that fraud is mean. It's that for 15,000 years fraud and shortsighted thinking has never ever worked -- not once. Eventually, people get caught. Things go south. When the hell did we forget all that? I thought we were better than this. I really did. And the fact that we're not doesn't make me feel all right and superior. It makes me feel sad. And as fun as it is to watch pompous dumb Wall Streeters be wildly wrong -- and you are wrong, Sir. I just know that at the end of the day average people are going to be the ones that are going to have to pay for all this because they always, always do.

Conference co speaker's immediate response to Mark Baum's comment:

"... in the entire history of Wall St. no investment bank has ever failed, unless caught in criminal activities. So, yes, I stand by my Bear Stearns optimism."

... Closing line:

Mark Baum "Paulson and Bernanke just left the Whitehouse.

There's going to be a bail-out.

They knew.

They knew the taxpayers would bail them out.

They weren't being stupid.

They just didn't care."

As falling U.S. home prices leave mortgage borrowers owing more than their homes are worth, borrowers are encouraged to stop paying the mortgage, move out of the house, and send the keys to the bank ("jingle mail"). That much is well known. But, as this Bloomberg story explains, the practice of selling and reselling mortgage loans, packaging them into securities and selling them again, and so forth, is enabling some borrowers to stop paying their mortgages and keep their homes, because nobody can prove to whom the money is owed. (Jingle Bells?) Presumably, if the borrowers can stay in the homes long enough, they eventually acquire ownership through squatting laws. (Jingle all the way?)

Defaulting borrowers don't need to be dishonest when resisting foreclosure. They only need to say: "I know I owe money to someone. But if I no longer owe it to the lender from whom I borrowed it, and if the present claimant doesn't have the paperwork for it, then I have no way of knowing to whom I owe it, and neither does the court." And that's the truth. But the borrower needs to be assertive. If the purported creditor pretends to have lost the mortgage note or offers a mere copy of it, and if the borrower doesn't question the claim, the court will rubber-stamp it. The borrower also needs to keep paying the property taxes, lest the government start separate foreclosure proceedings.

Of course, thanks to the alchemy of fractional-reserve banking, the money that is not returned to banks by stay-put defaulting borrowers will have the usual 12-times multiplier for the reduction in the banks' capacity to make further loans. The credit squeeze just got tighter.

Triguboff told the audience he was able to pay “very little tax”...

Triguboff told the audience he was able to pay “very little tax”...

"The cost to construct a given house is roughly the same in any region or metropolitan area of the United States. Yet, in the places were economic activity is robust and population dense, the land component of a residential property can equal 50 percent or more of the purchase price of a property. This occurs because the rent of land is lightly taxed and is therefore capitalized by market forces into a selling price, a selling price driven upward by speculation, hoarding and liberal access to credit. Henry George rightly observed that the rent of land should be fully collected by society to pay for public goods and services, leaving capital goods (e.g., buildings, homes, machinery) unburdened by taxation. If this was done, he felt confident there would be no need to tax income or commerce."

"The cost to construct a given house is roughly the same in any region or metropolitan area of the United States. Yet, in the places were economic activity is robust and population dense, the land component of a residential property can equal 50 percent or more of the purchase price of a property. This occurs because the rent of land is lightly taxed and is therefore capitalized by market forces into a selling price, a selling price driven upward by speculation, hoarding and liberal access to credit. Henry George rightly observed that the rent of land should be fully collected by society to pay for public goods and services, leaving capital goods (e.g., buildings, homes, machinery) unburdened by taxation. If this was done, he felt confident there would be no need to tax income or commerce."